“If you want to pay less taxes, read this book. Shaun teaches this simple truth: There are two types of tax seasons: Tax Planning season & Tax Paying season. Working with the Fuse team during tax planning season, you will keep more of your hard earned cash during tax paying season.” Harvee Pene

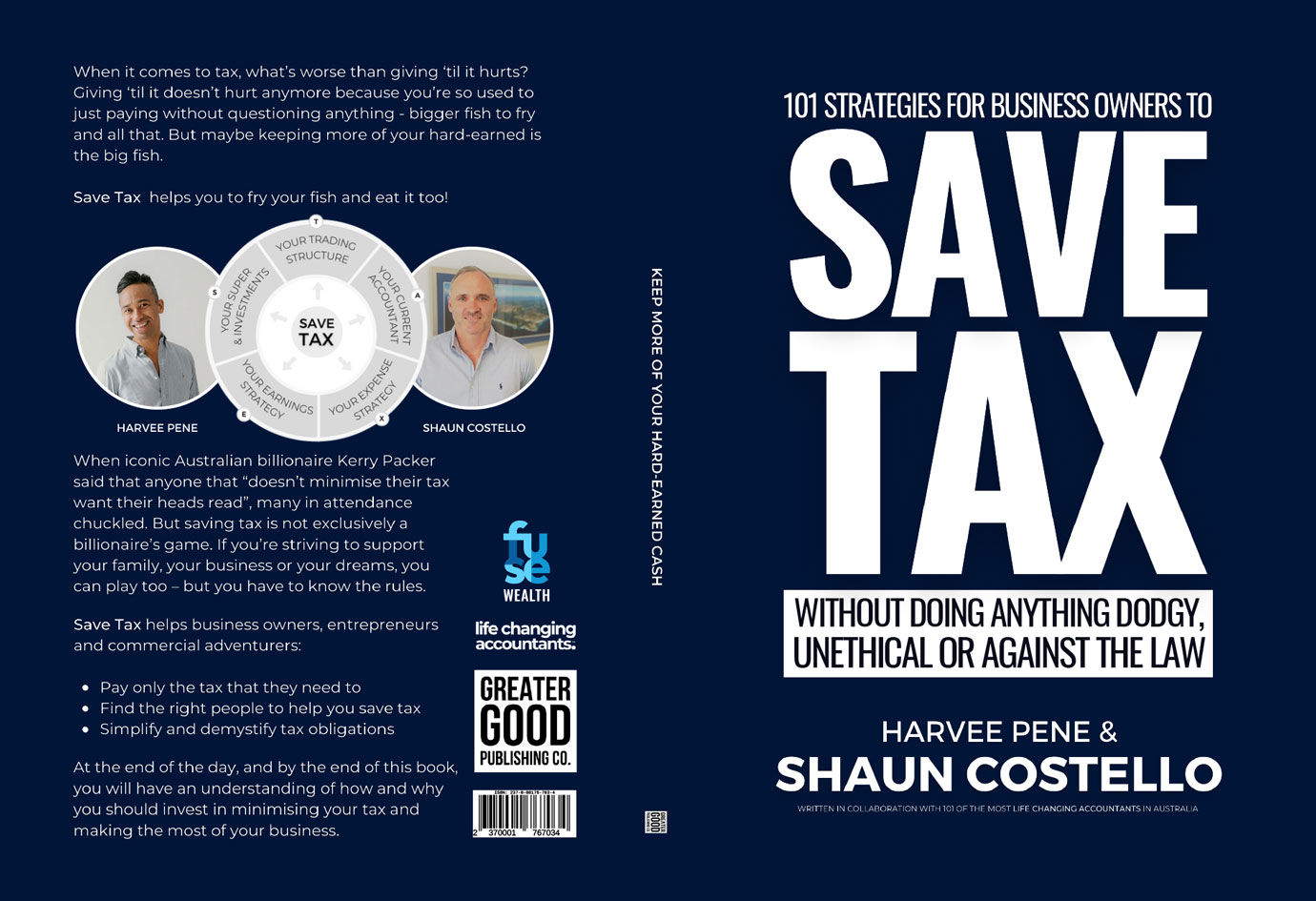

When it comes to tax, what’s worse than giving ‘til it hurts? Giving ‘til it doesn’t hurt anymore because you’re so used to just paying without questioning anything – bigger fish to fry and all that. But maybe keeping more of your hard-earned is the big fish.

Save Tax helps you to fry your fish and eat it too!

When iconic Australian billionaire Kerry Packer said that anyone that “doesn’t minimise their tax want their heads read”, many in attendance chuckled. But saving tax is not exclusively a billionaire’s game. If you’re striving to support your family, your business or your dreams, you can play too – but you have to know the rules.

Save Tax helps business owners, entrepreneurs and commercial adventurers:

At the end of the day, and by the end of this book, you will have an understanding of how and why you should invest in minimising your tax and making the most of your business.

KEEP MORE OF YOUR HARD-EARNED CASH … (OUT OF THE ‘TAX-MANS’ HANDS!)

We’re clear on the fact that we are measured by the pure value we create for and with you.

We want to help you create a business and a legacy that you’re proud of. One that brings you joy as opposed to stress and one that also does good in our world too.

Oh … and a business that really works … so you don’t have to work quite as much.

And so the impact on you, your family, our community and our world is inherently positive … Inherently good.

That’s why we begin with helping you keep more of your hard earned cash (out of the tax man’s hands!)

Saving Tax is essentially about one thing and one thing only – taking home more money to your family.

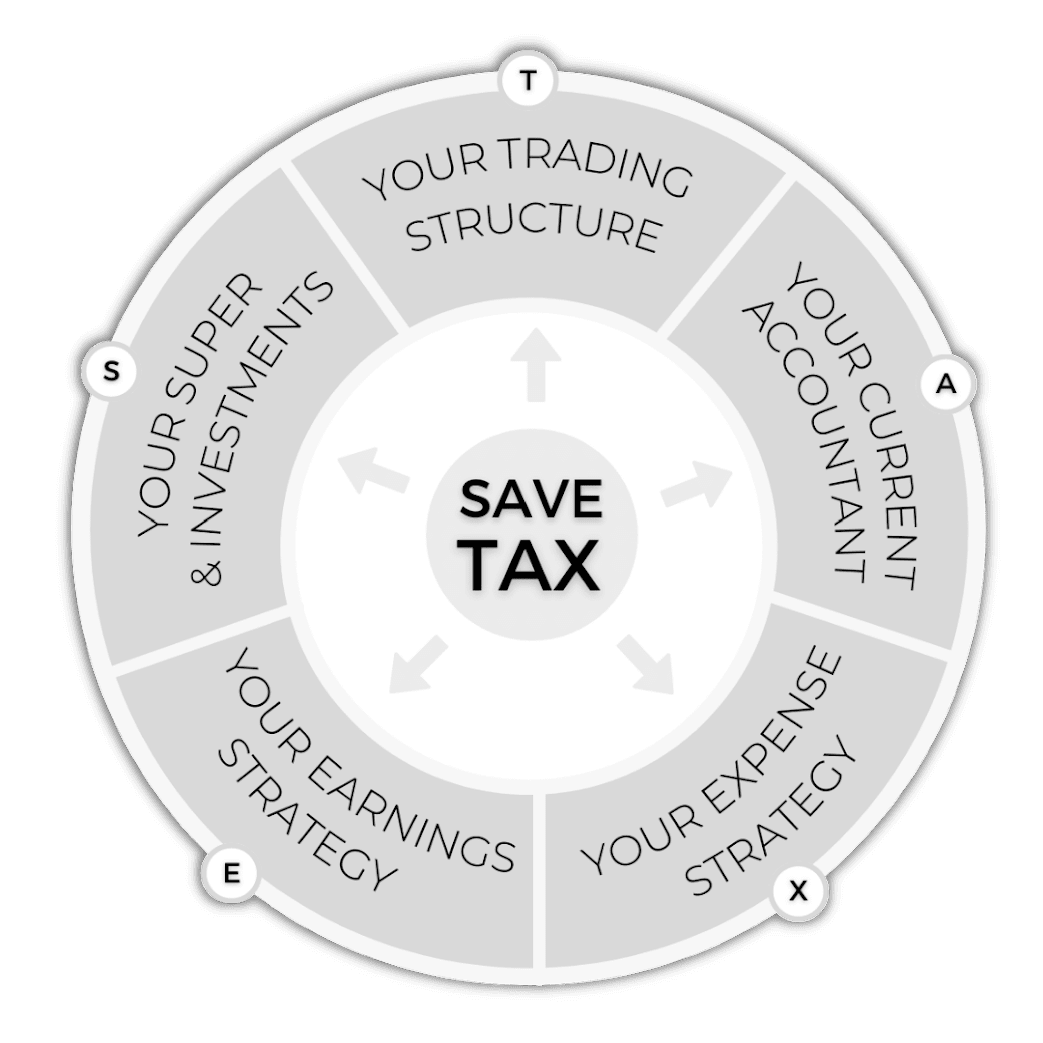

There are 5 key Tax Saving Criteria that each contain a number of 100%, squeaky-clean & cutting edge tax strategies will ensure you pay the least amount of tax legally possible.

T is for Your Trading Structure

Are you 100% sure your ‘structure’ is set up so that you’re not paying unnecessary taxes?

A is for Your Current Accountant

Have you recently made a large tax saving by planning it out in advance with your advisor?

X is for Your eXpenses Strategy

Are you sure that you’re applying every legally available tax saving strategy?

E is for Your Earnings Strategy

Do you know if you should pay yourself a salary, dividend, distribution, loan or something else?

S is for Your Super & Investments

Do you use Trusts, Companies & SMSF’s as your own legal ‘havens’ to pay less tax?

Hi! I’m Shaun Costello

As members of Life Changing Accountants, we’ve made a public commitment to be driven by one thing:

MAKING AN IMPACT

An impact on the businesses and lives of our clients, and together with them an impact in our communities and our world.

Our commitment, not surprisingly, is a total commitment to stand by the results that we create for our clients where –

- R is for … Greater Revenues

- E is for … Improved Equity

- S is for … Surplus Profits

- U is for … Supporting the U.N. Global Goals

- L is for … Reduced Liabilities

- T is for … Proactive Tax Savings

- S is for … Scaling Cashflow

SO THAT we can proactively help our small business clients reach ‘THE RESULTS BENCHMARK’ –

Here’s a Look at What You’ll Discover When You Get Your Signed Copy of The Save Tax Book …

(index of 101 Strategies to Save Tax)

- Don’t accept your tax situation. (Page 2)

- It’s best if you can get the trading structure right first time. (Page 16)

- Sole trader is easy and cheap, but it’s risk-laden. It also places restrictions on your tax planning ability. (Page 18)

- A company is the most popular structure, and for many it’s the only viable choice. (Page 18)

- A trust scores highly in tax savings, planning ability and protection — but it’s not for everyone. Check your suitability with a professional. (Page 19)

- See Chapter 5 for more detail on Earnings types. (Page 29)

- Spend the time and money now to get your structure right, because a restructure later can be painful and expensive. (Page 29)

- If you can, choose a structure in which you can separate business risk from personal risk. (Page 29)

- It’s no good saving money on set-up costs now if it means a lifetime of high taxes. On the other hand, it’s no good choosing a structure with great tax planning capacity if the cost of set-up sends you broke. (Page 30)

- Ask yourself what assets the business will own and dispose of. Talk to your accountant about the tax implications. (Page 30)

- Go back to point 2 above before you answer this. (Page 31)

- Consider your prospective clients/customers and make sure they’re okay with whatever structure you’re planning. (Page 31)

- Research your industry and consider your plans around activities like R&D and know your licensing requirements. Ask your accountant for advice. (Page 31)

- Be aware of the type, extent and cost of compliance demanded of each type before you choose. (Page 32)

- Remember, a really good ship is compartmentalised — if one compartment is flooded, the ship can still sail on! (Page 32)

- Make a roadmap of your future and consider all possibilities. (Page 33)

- Choosing the most effective trading structure is all about how you plan to manage your assets,grow, and the risks associated with your business. (Page 36)

- Both trading structure controllers have responsibilities and legal obligations. Choose your structure according to the role you’re most comfortable with. (Page 39)

- Choose the people who will fill these roles carefully. Seek advice. (Page 40)

- Discuss the impact of share classes on CGT with your accountant before making any binding decisions. (Page 40)

- Sometimes it becomes necessary to distribute income or assets from one trust to another that has made losses, and when that’s the case you’ll need to make an FTE. (Page 42)

- Talk to your lawyer about the legal and financial implications of having a trust and the impact on your will. (Page 42)

- If business seems to be booming, the earlier you restructure, the less it will cost you. (Page 43)

- Fast forward to “Chapter 5 — E is for Earnings” and the section on “9 ways to save tax when you’re selling your business” for a deeper look at these concessions. (Page 47)

- Weigh up all the costs, concessions, timing issues and risks of a restructure before you commit to it. If you can, undertake a comprehensive cost/ benefit analysis — your accountant should be able to help. (Page 49)

- In 2019 in Australia, the amount you earn determines which tax bracket you fall under. $90k was kind of that perfect balance between giving money in your name, being able to access loans, and paying tax without giving too much to the tax man. That’s the magic number we used but of course as profits, tax rates and your circumstances change so does the magic number. (Page 51)

- Where a lot of people go wrong, and a lot of accountants don’t explain what the effect of a trust distribution to a beneficiary is… the beneficiary has a legal right the the funds when called for so be very careful who you distribute to! (Page 52)

- You can also distribute to a second company that’s making a loss. So if you’ve ever had businesses that haven’t done so well, there may be a way to soak up some of those losses. (Page 53)

- Try and give the most to people in the lowest tax brackets first but be aware if your distribution changes their marginal tax rate. Best if you can have family members who are not earning at all, as the first $20,000 you distribute to them will be taxed at zero. (Page 58)

- If you distribute trust funds outside the specified individual’s family group when you have a family trust election in place, you will be hit with the Family Trust Distribution Tax (FTDT) which is payable at the top marginal rate or tax. Be careful. (Page 59)

- If you’re committing to a company structure, there are some issues to take into account including what shares to issue. (Page 61)

- There is a greater demand by shareholders for preference shares in start-up companies as they can receive assurance of recompense in cases of liquidation. (Page 66)

- Don’t make the decision on business trading structure on your own! Talk to your spouse, people who have been in your position, and most importantly, your accountant. If you don’t have an accountant you can trust to give you the right advice, the next chapter is for you. (Page 67)

- Every day you spend working with a dinosaur is costing you money. Remember back in Chapter 1 when we spoke about the power of compounding? Every dollar you pay too much in tax is a dollar that has the potential to turn into a fortune. (Page 73)

- Read my book ‘Become a Business for Good’ to learn more. (Page 77)

- I strongly advocate that planning for the end of the next financial year begins on 1 July every year. (Page 78)

- Find an accountant you trust and who delivers the informed proactivity you need and keep them close to you for the rest of your working life. (Page 80)

- Find the weak spots in your cash flow — clients who are slow in paying — and reassess your relationship with them. Do you really need clients like that? (Page 81)

- Now, physically separate these amounts of money. It’s as simple as setting up separate accounts for tax, operations and profits. (Page 82)

- Get audit insurance and sleep better at night. (Page 83)

- “If your current accountant hasn’t already apprised you of all of these deductions, you probably need to interview a few new accountants.” (Page 85)

- You need to be across the ATO’s definitions before you start making claims that can later come back to haunt you. (Page 91)

- The ATO is pretty understanding, but they’ll have a hard time accepting a claim for electricity used at the same time you’re claiming travel to a work site. (Page 92)

- If your business is all about personal services income, you may not be able to claim occupancy deductions. See Chapter 5, E is for Earnings to learn more. (Page 93)

- I always say “a bird in the hand is worth two in the bush” so unless you have a definite plan to sell the property soon, just take the deductions. (Page 94)

- Search ATO TR 9330 (or 93/30) for a downloadable PDF that will set you straight on these deductibles. (Page 94)

- You can apply a four-week representative period (in which you keep detailed records of things like phone usage, internet usage etc) to substantiate your claim for the year. But if your work patterns change, you need to create a new record. (Page 96)

- Consider whether the actual cost method will genuinely realise a greater deduction, and weigh the benefit against the cost of meeting the recording and calculation criteria. (Page 96)

- The $10 million (and expanded $50 million) thresholds don’t apply to CGT concessions (threshold $2 million) or the small business income tax offset (threshold $5 million). (Page 97)

- Check your eligibility for any and all of the above by accessing the ATO website and/or talking to your accountant. Remember, in taxland things change quickly, so what’s current for me at the time of writing may not be current for you. (Page 100)

- Don’t forget the luxury car limit — the current max deduction is around $60,000, and you can only claim for the business portion of use. (Page 101)

- Work with your accountant on this one to see what different valuations you get on the cost (purchase price) / market selling value / replacement cost of your stock. It may take a little time and effort, but it may be worth it. (Page 106)

- Always review your bad debts, and if they haven’t been paid, write them off. Otherwise, you not only miss out on the money you earned, you lost the tax you paid as well. (Page 107)

- Be sure and notify the ATO of your tax losses at the earliest opportunity. You could forgive the taxman for being suspicious if you suddenly “find” a loss in a previous year, when you’re having a boomer of a time this year. (Page 107)

- Your business structure dictates how your business losses are treated, If you are planning an early loss for your start-up business, talk to your accountant about the best structure for your purposes. (Page 108)

- In some circumstances, and providing you meet certain tests, it’s possible to use the losses in your trust with profits from other trusts. (Page 109)

- Depending on a range of factors, the carry back loss could result in a reduction of your debt to the ATO, tax credits, or — wonder of wonders — a tax refund. (Page 112)

- If your expenditure is less than $20,000 you can still claim the incentive if you engage a registered Research Services Provider (RSP) to conduct your research. (Page 113)

- There’s also a provision to claim depreciation on assets used in the R&D activity, but you can’t claim for the cost of acquiring or constructing a building, interest expenditure, or money spent on core technology. (Page 114)

- Be aware that there’s a danger of ‘double dipping’ here — if you’ve claimed an R&D incentive offset for certain expenses, you can’t then claim again on your company tax return. (Page 114)

- Driving the car from home to work and back is not considered business use, so don’t try to claim it. That sort of behaviour can make the ATO very suspicious of your other claims. (Page 117)

- To bring the FBT down further, an employee can make contributions to the running costs of the vehicle either by paying directly to the company or paying for the running costs themselves. (Page 117)

- There are exemptions from FBT for “minor and infrequent benefits” where the taxable value is below $300 per employee and the frequency of benefit provision is less than 10 times per annum. If the meal is provided on the premises on a working day, that is also exempt. (Page 119)

- If you go all out and have the spicy fish in banana leaves with a nasi goreng special and a serve of roti, and it costs more than the “reasonable amount”, you can still claim, but you just have to keep the receipt. (Page 120)

- Remember, you can only claim on those “reasonable amounts” if the allowance your employer has paid is part of your taxable income. If the allowance paid by the employer doesn’t show up as part of your taxable income, you can’t claim. (Page 121)

- Make sure that if you are receiving a share of business income from a partnership or trust, you are getting your offset. We have seen this overlooked too many times. (Page 122)

- Of course, if you have some sort of windfall or you’re restructuring, there’s no point in holding onto any debt you don’t have to — pay it all out and wave goodbye to interest. But ask your accountant first as offsetting your debt maybe a better option. (Page 123)

- To make the most of the tax deductibility of good debt, don’t “taint” it by repaying it. (Page 123)

- You may be tempted to make a bequest to a charity in your will. Good for you. But if you give while you’re alive, you get the tax benefits. Not so much when you’re gone. (Page 125)

- Capital works are deductible, so if you’ve built, altered a building or spent money on capital improvements to the surrounding property, you can claim. And that includes the cost of professionals such as engineers, architects and surveyors. (Page 126)

- There are numerous logbook apps available for your smart phone, which take some of the drama out of logging each trip. If you use one that records every single trip for the whole year, it can help you determine which 12-week period to use as the representative period. (Page 127)

- The important thing about PSI is that it doesn’t matter what sort of business structure you have in place, if your income is classed as PSI, the tax rules applying to it are applicable to you. (Page 135)

- There’s a handy Personal Services Income (PSI) decision tool on the ATO website, which will help you work out whether any of your income falls under the provisions of PSI. (Page 138)

- The trap here is that a lot of people are keen to escape from PSI-land so they incorrectly self- assess themselves as PSBs, and that can get you into trouble. (Page 139)

- Don’t forget that while you can draw money out of either a Company or a Trust, the way we treat that money for tax purposes is very different depending on which structure you are using. (Page 141)

- One advantage of a wage is that you can match your salary to your living costs pretty closely and stop seeing that company money as your own resource, which hopefully means it will end up in growing profits. (Page 142)

- In other words, the 7A rules don’t apply to trusts, making “drawings” or loans a more practical affair. (Page 143)

- You can’t afford to make any mistakes on documentation or compliance with the terms of a 7A loan. If you do, the whole of the loan becomes fully taxable, so you could end up paying way more than you might have saved. (Page 145)

- Not all shareholders are eligible for dividends — check the shareholder classes in ‘Chapter 2 — T is for Trading Structure’ for more details. (Page 146)

- If your company is making good profits, it’s important to regularly ‘empty out’ the retained earnings in a trading company, otherwise it could become a juicy target to be sued by creditors or disgruntled employees. (Page 147)

- And don’t forget, you need to work your distribution structure out before the financial year ends, or you could be in all sorts of strife with the ATO when it comes tax time. (Page 148)

- Always check your franking account before you pay dividends from the bucket company. (Page 149)

- There’s a fair amount of compliance around this strategy, with a requirement for a shareholders’ resolution being made, so it’s probably a bit arduous to pull off unless there are large amounts of money involved. (Page 151)

- Just beware that the ATO might get suspicious if your 14 year old is earning a full $20,000 for sweeping, which coincidentally uses up their whole tax free threshold. (Page 152)

- Beware — the 50% CGT discount does not apply if the asset is owned by a company. (Page 154)

- It’s worth noting that these small business CGT concessions are only for business assets, not for passive investment assets like listed shares or residential rental properties — but can include commercial property that was used in the running of your business (unless held by an SMSF). (Page 157)

- If you mess these up, it may cost you hundreds of thousands in tax that you didn’t expect to pay. So don’t say I didn’t warn you to get the advice! (Page 159)

- Be careful to not exceed your ‘Contribution Cap’ for deductible superannuation contributions because going over the caps mean you could pay an effective tax rate of 47% in tax. Ouch! (Page 161)

- Private Health Insurance (extras cover) does not remove the surcharge — you must have hospital cover. (Page 162)

- Donating or “tithing” to Churches cannot be claimed as a tax deduction on an individual tax return unless they are a DGR. You can search the Australian Business register to see if your intended recipient is a DGR. (Page 163)

- If you have a large amount of debtors (money owed to you), under accruals rules you pay income tax on that money even though you haven’t received it yet. (Page 170)

- ” get the advice of a qualified expert such as a financial advisor before you implement any of these measures.” (Page 173)

- Both the income the super fund earns and the income you receive from your pension are tax free when you implement this stRategy. Unless you’re under 65 and taking a Transition to Retirement (TTR or TRIS or TRIP) pension, in which case both the fund’s income and your pension payments are taxable at 15%. (Page 177)

- If you’re eligible, the government will make that determination when you lodge your tax return — you don’t have to do anything. (Page 180)

- Just remember, an in specie asset transfer into an SMSF effectively removes access to the asset until you reach your preservation age, so be sure you won’t need to access your transferring assets before then. (Page 183)

- You can also use your SMSF to buy other properties, including rental properties. (Page 186)

- The advantage? As your principal place of residence, when you sell it, you pay no capital gains tax even though you have rented it. Woo hoo! (Page 188)

- Just beware that when you sell, the capital gain will fall to the nominal owner, and that may change their tax situation. (Page 189)

- Early repayment penalties for variable rate loans are effectively now banned, so if you’re planning to refinance, sell, change or payout the loan within the fixed rate loan term you’re contemplating, consider a variable rate loan instead. (Page 190)

- Isn’t it worth spending a few hundred bucks on a report that will gain you thousands in extra depreciation claims? (Page 192)

- Take a hard look at those assets that have a bleak future and sell them if you foresee a capital gain on some of your other investments. you can offset the gain against the losses made. (Page 192)